%20(1).png?width=469&height=405&name=Group%2023%20(2)%20(1).png)

The Catch-22 of In-House Tracking

Keeping your tracking in-house allows you to control borrower communications with no vendors to manage.

But that DIY responsibility using manual workflows can complicate every tracking task and lead to missed mailing requirements, compliance mistakes, and audit worries. In addition, the unchecked flow of borrower frustration is directly focused on your loan servicing staff and even reaches upper management.

.png?width=455&height=417&name=Group%2024%20(1).png)

Publically Traded Insurance Tracking

Their big name suggests that you'd get access to better software, real expertise, and the prestige that comes with name recognition.But they've lost what no lender can afford to ignore: their focus on borrower relationships and personal attention to the needs of your institution. Big promises can result in treatment you'd never give a borrower: like just another number.

.png?width=465&height=473&name=Group%2025%20(1).png)

The worst of both worlds: Legacy Tracking Software

Tracking software is supposed to streamline servicing operations and free up staff time for work that needs actual human attention.But legacy tracking software isn't capable of keeping up with the demands of new regulations or complex multi-collateral loans. Paired with a legacy approach that feeds on excessive false placements, your bank or credit union can end up with the worst of both worlds: constant data clean-up, the loss of direct control with borrowers, and continued borrower noise.

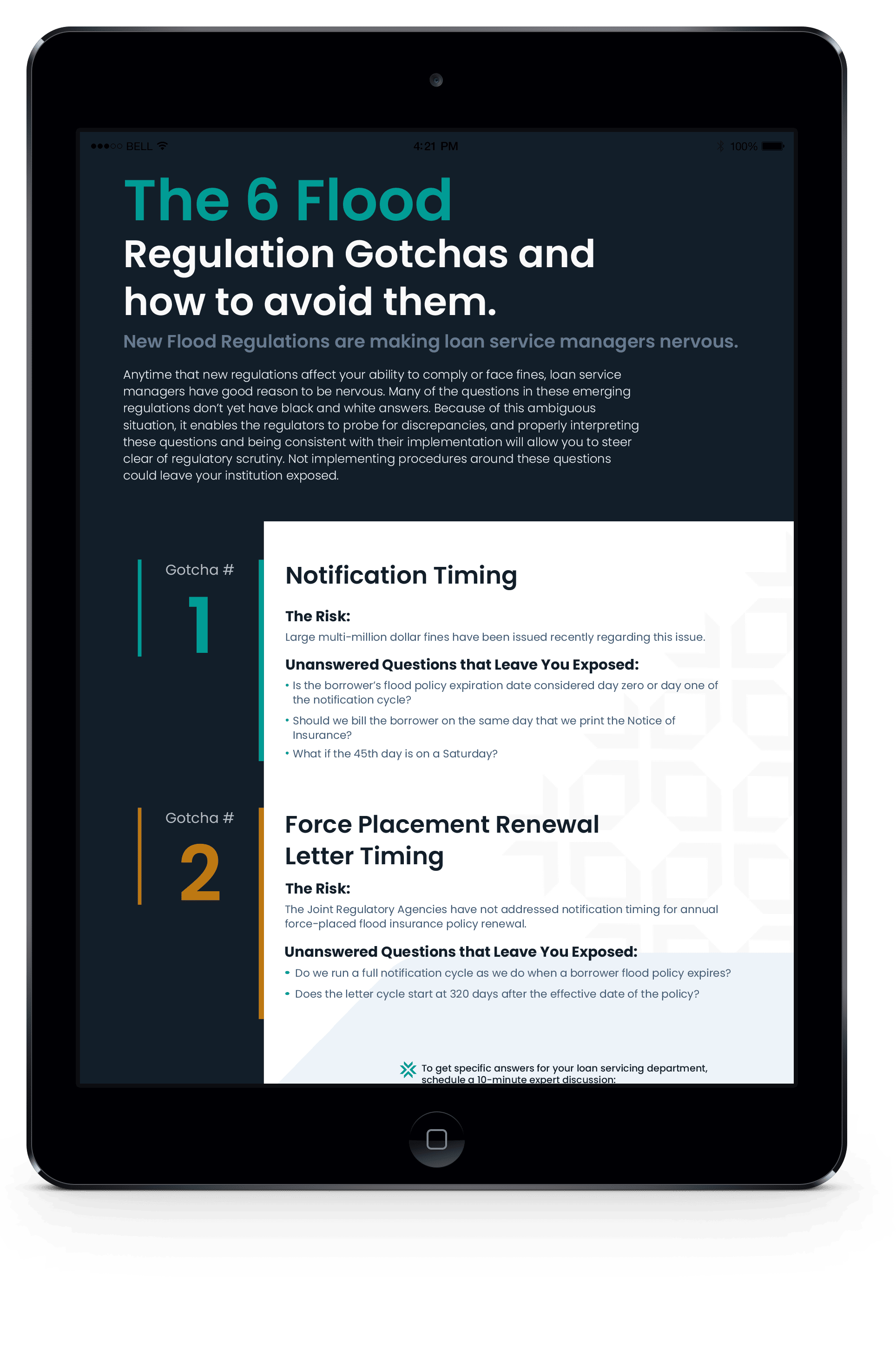

Top 6 Flood Insurance Gotchas

x